The US hospital professional liability (HPL) environment is undergoing a profound transformation, marked by a significant increase in the financial magnitude of jury verdicts and settlements. This shift directly impacts HPL underwriters by escalating potential payouts and increasing the overall risk profile of healthcare institutions. The average value of the top 50 largest medical malpractice verdicts in the US has dramatically increased, more than doubling from $27 million in 2019 to $56 million in 2024.

This sharp acceleration, particularly noticeable following the slowdown of US courts during the COVID-19 pandemic, underscores a critical shift in the financial exposure faced by healthcare providers and, consequently, their insurers. This trend signals a new and more challenging era for risk assessment, limit profiles, and premium setting.

Historically, HPL underwriters have focused on the insured’s medical treatment and patient acuity to gauge potential losses in the excess liability layers. And while the verdict trends described above are specific to “medical” liability, the concern of underwriters has turned toward the risks associated with sexual misconduct. The severity of sexual misconduct cases dwarfs the verdicts/settlements of its medical malpractice counterparts. These cases collectively demonstrate persistent systemic failures in institutional oversight and accountability, resulting in hundreds of millions or even billions of dollars, underscoring the severe economic consequences for healthcare organizations.

The Medical Professional Liability Association (MPL Association) released its 2024 Financial Results Analysis and 2025 Financial Outlook, which outlines the industry's key financial metrics for 2024, most notably financial performance (combined ratios), premium growth, accident-year loss ratios, and reserve changes in prior accident years. One item to note is that the MPL Association’s review of the hospital sector showed a year-over-year premium growth higher than any other healthcare sector (despite a shrink in licensed/staffed beds during the same period). It should be noted that a large portion of the HPL results for premium and losses are not shown in insurance companies’ statutory annual filings.

Of the 50 largest hospital systems in the US, a majority utilize offshore captives that are then reinsured by international/domestic HPL carriers. The captives’ premiums, their losses as well as the results of the carriers that reinsure them, are not found in the annual statements for direct insurance. In short, the medical professional liability insurance industry is still performing at a combined ratio of greater than 100%, but this statistic does not contemplate some of the largest malpractice and sexual misconduct payouts.

Whether through direct liability or vicarious, hospitals and their HPL insurers are handed most of the healthcare industry’s nuclear verdicts. Due to their extraordinary financial magnitude, these verdicts and final settlements pose significant challenges for HPL underwriters. Most industry reports suggest that medical malpractice claim frequency is flat over the past five years; however, the number of multiple-claimant, sexual misconduct claims/incidents has grown.

The escalating severity in medical malpractice coupled with the frequency of sexual misconduct liability necessitates a fundamental re-evaluation of traditional underwriting models. It demands a heightened emphasis on catastrophic risk assessment, a recalibration of capital requirements/capital deployment, and the proactive implementation of robust risk mitigation strategies within insured hospitals.

Let’s look at both the frequency and severity of sexual misconduct liability events in hospital/health system settings. A 2023 Joint Commission study found:

- Incidents of assault, rape, sexual assault, and homicide increased by 77% over a two-year period and have steadily risen over a five-year period (See Figure 1 from the Joint Commission study).

- Out of 1,411 sentinel events in 2023, assault/rape/sexual assault/homicide was 8% of the total adverse events (n=106), as seen in Figure 1.

- As stated in the study, “Sexual assaults including rape comprised 43% of violence-related events, with 50% occurring patient-on-patient, 28% staff-on-patient, and 13% patient-on-staff.”

Figure 1

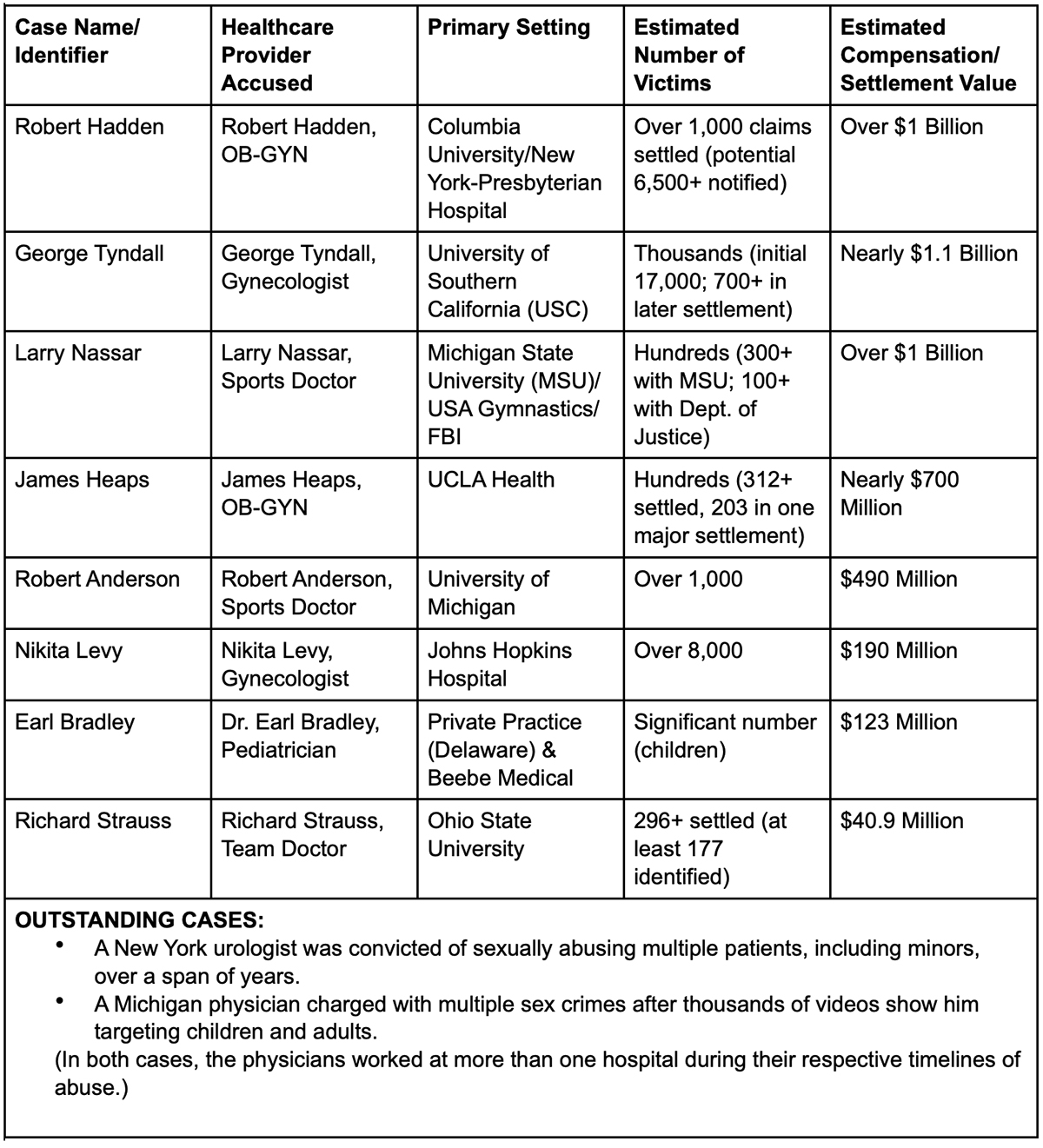

To understand the volatility of the growing number of sexual misconduct liability cases, we should look at some of the largest verdicts and settlements that have hit the hospital sector (see Table 1). When considering these values, consider that there were varying portions of insurance and self-insurance between the commercial market and the health systems where the injuries occurred.

Table 1: Overview of Major Sexual Misconduct Cases in US Healthcare Settings

The 2023 Joint Commission report indicates only 30 cases of staff-on-patient sexual assaults occurred (28% of 106). While 30 out of 34.4 million hospital admissions seems like an insignificant figure, the ultimate resolution of these cases exhausts a hospital’s self-insured retention, all available limits of insurance, and in some cases, requires additional (uninsured) payments by the defendant(s). There are loss projections that indicate 15 open cases during the 2022-2024 period could result in $500 million to $1 billion in losses by insurers and reinsurers. Unfortunately, in a very niche market, there is a small number of insurance carriers who will share these losses and an even smaller number of reinsurers.

With such a small number of offenders drawing the attention of HPL underwriters, we often forget the key focus of this insurance is to protect against professional errors. Excess HPL carriers have to quantify the probability of a large professional loss(es), in addition to losses associated with sexual misconduct liability events, and in some placements, excess auto liability events. This is no easy task when you consider the growing severity associated with just the professional liability.

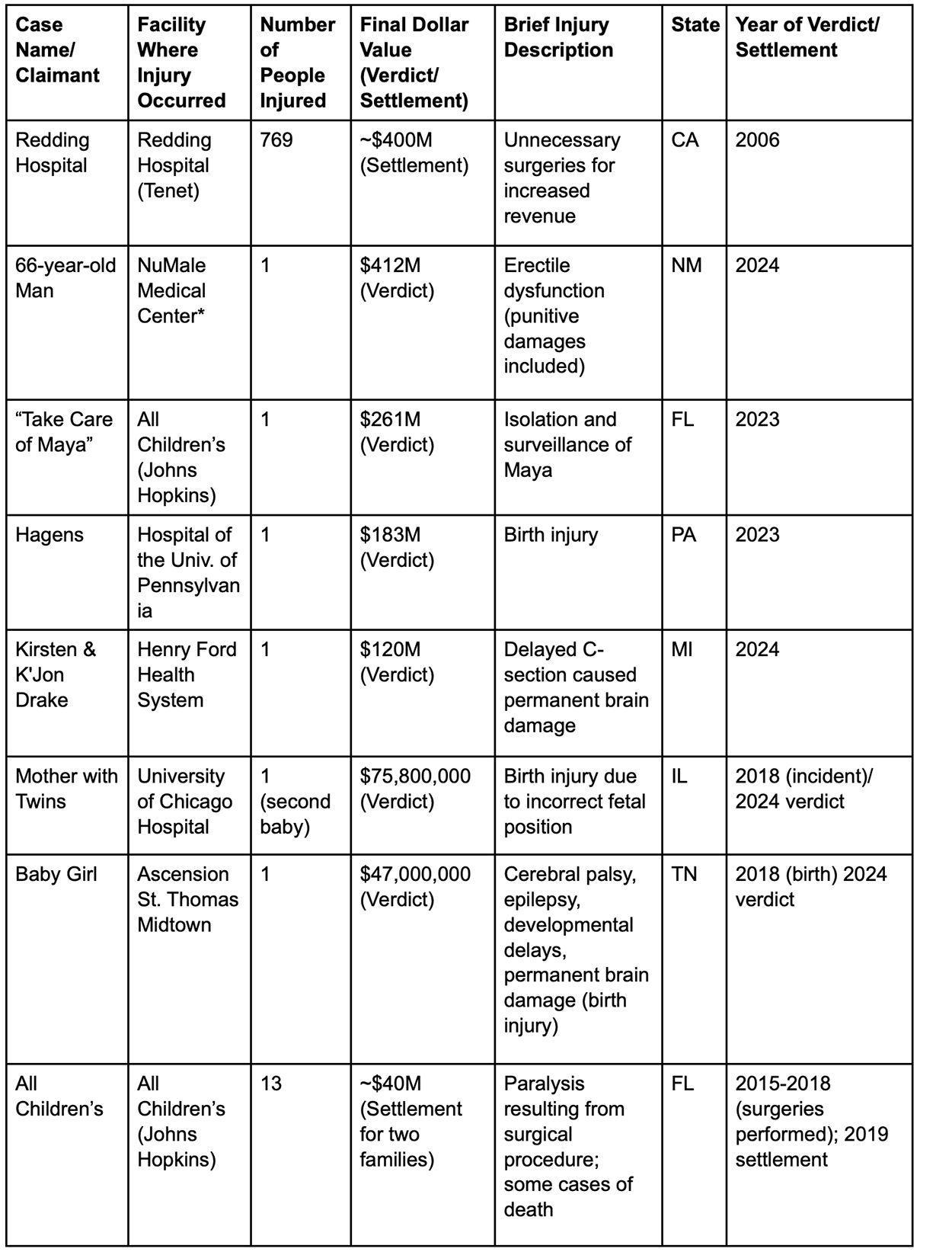

Table 2: Overview of Major Malpractice Cases in US Hospital Settings

* NuMale case did not occur in a hospital setting. It has been included to show the growing severity for a service often provided by a hospital/health system.

An analysis of these high-value medical injuries does not clearly identify reoccurring patterns that can be addressed with risk management. When reviewing a larger sample of cases, patient acuity and venue are critical factors to consider. On the other hand, the sexual misconduct cases reveal several consistent and alarming patterns that can be addressed with patient safety and future prevention strategies.

The HPL market needs to start treating Excess Hospital Liability like large, property catastrophe (CAT) coverage: Event, Hazard (or Intensity), Vulnerability, and Financial.

- The Event Module incorporates different catastrophic events and calculates their potential damage, drawing data from history, geology, geography, or even psychology. (Most carriers are using log normal distribution models based on an insured’s 10-year experience and/or aggregated industry reports.)

- The Hazard Module or Intensity Module evaluates the risk of a particular hazard to a specific geographical area. (Professional liability claims’ severity often has a direct correlation with the court venue. Geographical adjustments are constantly made to pricing models, but the past few years have seen excessive verdicts outside of the typical “Judicial Hellholes.”)

- The Vulnerability Module estimates the damage to buildings and other properties from a specific hazard, with allowances made for local architecture and the stringency (or laxness) of building codes. (There is a positive correlation between the acuity of services and the severity of a loss. In sexual misconduct cases, it is the “vulnerable patient population” that is repeatedly injured.)

- The Financial Module estimates the cost of repairing damages caused by given events and designates who would be responsible for covering those costs. (The financial module in this sector is ultimately the hospital with the deep pocket. Projecting costs takes a team of medical experts, financial consultants, etc. A single claimant, with severe injuries, who requires a life care plan, in a venue without caps, can easily reach $25 million as a plaintiff verdict.)

And like Property CAT programs, we can envision a stable insurance market’s response where:

- Placements are syndicated with several capacity providers and no single market takes an excessive amount of risk.

- Insurers/reinsurers will find their respective sweet spots for attachments, rate-on-line, etc.

- Hospitals find alternative structures to procure insurance above “Per Claimant” retentions, or excess insurance with a Coinsurance Provision.

- Risk engineers must be used to assess the systems in place to mitigate loss.

If we are going to compare Excess HPL business to Property CAT Coverage, then sexual misconduct litigation is somewhere between California earthquakes and wildfires. Sexual abuse has represented a disproportionate number of multiple-claimant cases. There are no clear indicators for identifying a predator; none of the more notorious cases included someone who was on a sex offender registry. In sexual medical liability suits, geographic location has little to do with the financial module. But we can have risk engineers perform a more detailed review of protocols and set a new standard for risk tolerance.

Many of these cases have a prolonged nature of the abuse, often spanning decades before being fully exposed and addressed. This is evident in the cases of Hadden, Tyndall, Strauss, and Heaps. In most facilities, there are systems in place to prevent long-term abuse. Unfortunately, best practice protocols are not in all hospitals. The introduction of medical chaperones over the past decade has improved healthcare settings, but in many cases, checks and balances only reduce the years of abuse from 20 years down to two years. With average settlements per patient continuing to grow, a shortened period of abuse can still result in negative publicity (reputational risk) and compensation to victims in excess of $100 million. Despite the hard work occurring in these institutions, vulnerable patients continue to be victimized.

To effectively prevent future sexual misconduct in healthcare, HPL underwriters must work with their insureds to develop a multi-faceted approach incorporating robust prevention strategies. This should include:

- Highly protective chaperone policies

- Robust patient education and informed consent processes

- Clear documentation guidelines

- Safe and confidential reporting systems

- Comprehensive screening and background checks

- Environmental design

- Regular, interactive training

Hospitals have all the above protocols/procedures in place. The problem is the varying levels of prevention over the past 20 years, and the different levels of protection from one facility to the next. Collectively, we have to set new standards.

- Many health systems have “opt-in” policies that give patients the right to ask for a chaperone. That may be communicated in various ways, by signs in the exam room, a verbal offer by the provider, or in pre-visit handouts. However, this puts the burden on the patient to speak up and protect themselves in advance of an exam. Most patients simply trust their provider and don’t want to communicate mistrust by asking for a chaperone. Systems with “opt-in” chaperones for sensitive exams are the least protective. Opt-in policies are better designed for non-sensitive or near-sensitive exams out of respect for a patient who requires additional support or has experienced past abuse or trauma.

- Hospital systems that have experienced tragic events and learned the hard way are more protective of patients and providers by implementing “opt-out” policies at a very minimum. They make it the standard of care to automatically have a chaperone present for sensitive exams. If a patient wants to opt-out, they explain the standard of care, have both the provider and the chaperone document the patient’s refusal and have the patient sign an informed declination. There may be times when the provider exercises his or her right to defer care.

- Stricter protections need to be in place to address the needs of patients under sedation, those with impaired mobility, individuals in psychiatric settings, and especially children. There are some populations/examinations where a chaperone must be in the room. Mandatory chaperone policies are found in the most protective health systems. They do not allow the patient or family to opt-out of chaperones for sensitive exams involving especially vulnerable patients. When patients or families refuse a chaperone, the provider has the right to defer care except in an emergency.

- Consistent and unwavering accountability is needed from leadership and across all levels of the organization. Every health system employee should be a mandated reporter by policy, even those who are not legally required to report per applicable licensing boards. All allegations of misconduct must be investigated promptly, thoroughly, and impartially. Investigations should be conducted by trained, objective personnel, and appropriate disciplinary action must be taken against offenders, regardless of their rank or tenure. Too often investigations are done by someone who supervises or is in the same setting as the provider. It is hard in such cases to show impartiality. In systems where there is a corporate risk management department that oversees multiple settings, allegations should be escalated directly to the corporate risk management department.

- Patient education and informed consent is an extremely important step in preventing abuse. In many cases perpetrators were able to abuse multiple patients because those patients did not know what to expect during their examinations. Systems have learned the hard way that giving physicians the autonomy to explain the exam or treatment themselves at the time of the appointment is the least protective measure for preventing abuse. A more protective health system will make sure that patients are informed in advance of their visit what to expect in each type of medical appointment, including the standard use of chaperones when the visit includes sensitive examinations. Knowing in advance what to expect and that the standard of care includes a chaperone for sensitive examinations normalizes protective care, resulting in patients and healthcare professionals who are better equipped to speak up when there is a deviation.

- Institutions must commit to transparency by accurately tracking and reporting all incidents of sexual misconduct. This data should be regularly reviewed and analyzed to identify patterns, trends, and systemic weaknesses. But in addition to actual incidents, breakdowns in protocols need to be measured. An underwriting question might be: “Does your facility monitor the number of ‘opt-out’ of chaperone events per healthcare provider?” Without measuring when and where patients are opting out, a provider can go undetected and coax patients out of the protection they deserve.

Analyzing cases from hospitals, university health centers, and private medical practices (e.g., Copperman and a $1.6 billion verdict) under "hospital settings" is relevant for data collection but it also speaks to juries interpreting "institutional liability" broadly, extending it beyond the confines of traditional accountability. This expansion of accountability, the significant increase in the number of victims coming forward, often years or decades after the abuse (e.g., enabled by New York's Child Victims Act and the Adult Survivors Act), increased public awareness, and the collective impact of high-profile cases is a collection of trends that cannot be overcome with rate increases alone. There needs to be a shift in the entire risk framework. Large property underwriters use loss control services to catch poor maintenance, weak valuations, or unmodeled exposures, risks that brokers generally don’t surface on their own. HPL underwriters should leverage clinical risk management for chaperone audits, vulnerability assessments, and behavioral indicators.

Obstetrics was historically the service line every HPL underwriter wanted to hear about. A facility would describe their work with American College of Obstetrics and Gynecologists Fellows and an underwriter would feel comfortable with their awareness of patient safety. Based on some of the largest malpractice settlements, underwriters were right to focus on a facility’s OB department. But we cannot focus on one or two specialties to qualify and quantify the risk of an excess liability loss.

The healthcare and insurance industries combined must revisit excess hospital professional liability and how we protect against catastrophic losses. First, we must embrace some of the simplest rules of patient safety. Risk mitigation strategies specific to sexual misconduct must be re-examined, and historical exposures (gaps in protocols, inconclusive investigations, etc.) should be reassessed. We can all work toward best practices today, but that does not make the actions of a predator from five or 10 years ago disappear. So, if the HPL market and its policyholders are going to assume this risk of prior acts, we need underwriting models that assume “X” number of catastrophic events. And with a CAT model approach, insureds and HPL underwriters will discuss how sexual medical liability risk is shared, and how capital is deployed for a single risk versus a 20-hospital system.

A somber reminder to conclude: It is easy to become fixated on the dollars highlighted through this presentation. The most important numbers are the number of patients/victims. The documentary “At the Heart of Gold: Inside the USA Gymnastics Scandal” shows Rachel Denhollander, the first to publicly accuse former physician Larry Nassar of sexual abuse, addressing the court after more than 150 women and girls read their own victim impact statements: “When institutions create a culture where a predator can flourish unafraid.… This is what it looks like. It looks like a courtroom full of survivors who carry deep wounds…. Women and girls who carry scars that will never fully heal….” Some patients will have ongoing medical needs for the rest of their lives. Some victims will live with post-traumatic stress syndrome. One of the victims said, “I get scared and uncomfortable when I have to go to the [doctor's office]. I get scared I’ll be taken advantage of once again by another doctor.”

This year, a woman in Jacksonville, Florida, won a $25 million jury award in a hospital sexual abuse case (a confidential settlement was reached). The victim had to repeatedly tell staff about the predator. We can only hope that this was an isolated case. Let’s learn from this and other events. Sexual abuse in protective medical settings is preventable. We can once again make patients feel safe, and our healthcare institutions will avoid bankruptcy from a preventable risk.

References

ACOG Committee Opinion No. 796: Sexual Misconduct. (2020). The American College of Obstetricians and Gynecologists. https://www.acog.org/clinical/clinical-guidance/committee-opinion/articles/2020/01/sexual-misconduct

American Academy of Pediatrics. Use of Chaperones for the Pediatric and Adolescent Encounter: Policy Statement (2025). https://publications.aap.org/pediatrics/article/155/6/e2025071810/201949/Use-of-Chaperones-for-the-Pediatric-and-Adolescent

Best Practices for Sensitive Exams. (2019). American College Health Association. https://www.acha.org/documents/resources/guidelines/ACHA_Best_Practices_for_Sensitive_Exams_October2019.pdf

5 Crucial Steps to Take Now for Sexual Abuse and Molestation Safety in Healthcare. (2025). Michelle Foster Earle. https://www.linkedin.com/pulse/5-crucial-steps-take-now-sexual-abuse-molestation-sam-foster-earle-yiddc/

Sentinel Event Data 2023 Annual Review. Joint Commission Online.

2024 Financial Results Analysis and 2025 Financial Outlook. The Medical Professional Liability Association.