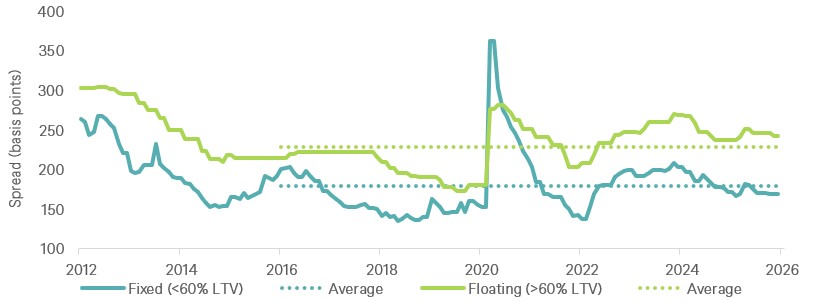

Real Estate Lending Spreads Appear Attractive on Historical Basis and Relative to Corporate Credit

We believe yield potential for real estate credit remains highly compelling. While real estate lending spreads have come down from their highs during the COVID-19 pandemic (2020) and following the onset of the Fed’s rate-hiking cycle (2023) (see Exhibit 1), they continue to hover near 10-year averages, offering compelling value relative to corporate bonds, in our view.

For example, spreads on fixed-rate <60% loan-to-value (LTV) loans average 170 basis points (bps), compared with 80 bps for investment-grade corporate bonds, a 90-bps premium (see Exhibit 2). To be sure, private real estate credit typically carries an illiquidity premium relative to listed bonds, but the gap is historically wide today.

Moderate‑leverage floating rate loans currently offer spreads of approximately 250 bps (see Exhibit 2)*. With modest leverage, these spreads potentially can rise to 400–500 or higher, with lenders typically receiving an additional 100–150 bps in upfront origination fees (Cushman Wakefield and DWS as of Dec. 2025). With the SOFR curve pointing toward a 3-3.25% landing, we believe all-in coupons will likely remain elevated relative to long‑term averages, even if short-end rates continue to decline (Cushman and Wakefield as of Dec. 2025).

*Bloomberg (corporate spreads); Cushman Wakefield (real estate lending spreads). Weighted by sector: Industrial (35%), Residential (30%), Office (20%), Retail (15%). As of December 2025.

Exhibit 1: Real Estate Lending Spreads

Source: Cushman Wakefield, weighted by sector: Industrial (35%), Residential (30%), Office (20%), Retail (15%). As of December, 2025.

Exhibit 2: Asset Class Credit Spreads

Sources: Bloomberg (CMBS); Bank of America (bonds); Cushman & Wakefield (real estate loans, weighted by sector: Industrial (35%), Residential (30%), Office (20%), Retail (15%). As of December, 2025.

We Believe Reset Values and Strengthening Fundamentals Provide an Attractive Entry Point

While corporate credit spreads are historically tight and equity markets are near all-time highs, real estate values still remain below peak values, and more in some sectors (notably Office)1. Accordingly, investors can originate loans at substantial discounts to replacement cost—to which our analysis indicates values typically converge over time—potentially reducing the risk of collateral impairment, which refers to a drop in the value of the property securing the loan.

The disparity between values and replacement costs has also curtailed construction (developer profit margins have been squeezed) and starts are down by 55% from their recent highs (see Exhibit 3)2.

Meanwhile, we believe that a growing economy and structural drivers (prohibitive housing costs, e-commerce, service-driven demand, and a return-to-office for the residential, industrial, retail, and office sectors, respectively) should support leasing activity. This combination of limited supply and buoyant demand will, we believe, create a favorable operating environment for borrowers, supporting rent growth and debt service coverage.

Exhibit 3: Real Estate Construction

Source: CoStar. As of December 2025.

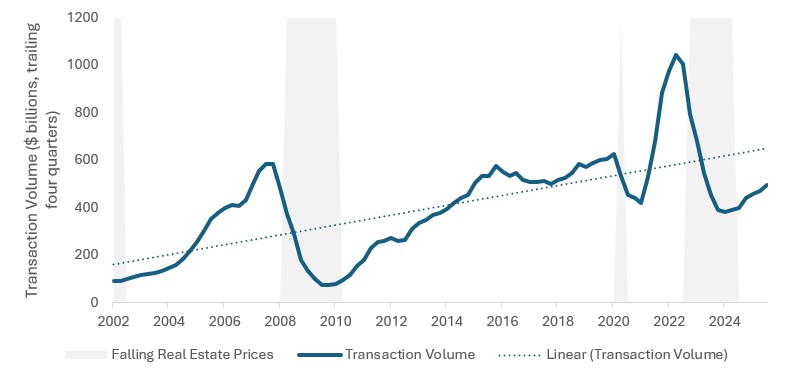

A Refinancing Super-Cycle and Resurgent Transaction Activity May Fuel a Multi‑Year Wave of Lending Opportunities

A powerful force shaping the real estate credit landscape is the sheer scale of upcoming debt maturities. Over $2 trillion of US commercial real estate loans are scheduled to mature between 2026 and 2030 (Mortgage Bankers Assoc. as of Dec. 2024). Many of these loans were originated in 2021 and 2022 when interest rates were near zero and valuations higher than they are today. As these loans come due, many borrowers will likely face a shortfall between their existing loan balances and what traditional lenders are willing to advance, especially given today’s more conservative underwriting standards.

A substantial volume of loans has already been extended, indicating that the refinancing cycle is only beginning. As those extensions expire, we believe that refinancing needs will accelerate meaningfully, while borrowers facing valuation resets or unfinished business plans will require bridge or transitional financing. At the same time, transaction activity is positioned to pick up meaningfully in 2026 as well, in our view: as base rates have drifted lower and price discovery improved, buyers have stepped back into the market (see Exhibit 4).

Exhibit 4: Real Estate Transaction Volume

Source: MSCI. As of December 2025.

While demand for capital is rising, the supply of capital from banks remains constrained. National banks increased their lending activity in 2025, but overall bank participation in the commercial mortgage lending market remains well below pre‑2022 levels, particularly among regional and community banks who are still working through legacy exposures and heightened regulatory scrutiny. We believe that private lenders have been and can continue to be the beneficiaries of the pullback, as borrowers seek lenders capable of delivering flexible structures, rapid execution, and transitional capital that banks are not positioned to provide. According to MSCI, the investor-driven share of commercial real estate lending activity more than doubled from less than 6% in 2020 to more than 14% in 2025.

To the extent that banks remain active in real estate debt markets, regulatory considerations incentivize them to deploy capital indirectly versus lending on balance sheet. Directly originated loans often come with ~100% risk‑weighting for senior mortgages and ~150% for construction or higher leverage loans. Instead, banks are increasingly choosing to extend credit to private lenders, where exposures often receive risk weights between 20-40%. This makes lending to private credit vehicles more capital-efficient and can generate a significantly better return on equity, even at lower spreads. For private lenders, it means more competition among senior financing providers, more attractive borrowing terms and highly accretive leverage that can potentially amplify returns without adding asset‑level risk.

Insurance Company Considerations

In an insurance investment context, real estate exposures—both private and public equity and debt—have been used by insurance companies for years. These have tended to fit somewhat specific roles: whether as investment grade bonds (e.g., mortgage backed security), high-income growth assets (e.g., private real estate equity) or longer-duration spread assets (e.g., commercial mortgage loan). In our view, more general real estate debt strategies are emerging as a new foundation of the extended core portfolio space that accepts lower liquidity and somewhat higher credit risk but may benefit from relative superior spreads, differentiated collateral based diversification, and stronger collateral strength than lending based on business risk (e.g., corporate high yield). This combination of income, structural protection, and diversification, which compares favorably against similar asset classes, is why we think real estate debt is of increasing interest to insurance companies.

From a portfolio construction standpoint, real estate debt can potentially improve diversification because its return drivers reflect both credit fundamentals, potential credit enhancement structures, and property-level collateral dynamics. As seen in this report, a supportive backdrop of attractive low-loan to value lending spreads, reset property values and a large refinancing pipeline, creates a strong tactical favorability to real estate debt beyond the strategic considerations above. Our analysis points to that taken together, these findings suggest real estate debt is most compelling as a near-investment-grade diversifier, but depending on company strategy, could also include, e.g., senior commercial mortgage loan and high-quality commercial mortgage-backed securities, which continue to offer insurers ways to potentially capture spread and collateral protection while tailoring portfolio construction to liability profile and regulatory capital considerations.

Conclusion

Together, these dynamics create what we view as a uniquely compelling setup for real estate credit: attractive spreads, reset valuations, improving fundamentals, and rising loan demand—all unfolding while banks remain selective, creating a potentially deep and durable opportunity set for private lenders. Against this backdrop, we see 2026 shaping up as a standout year—one where disciplined lenders can potentially capture compelling risk‑adjusted returns while supporting the next phase of the market’s recovery.